$1,000/month property taxes? Wow!Yeah this is what I meant to bring up earlier but got distracted. Health care for 2 will be about $2000/month conservatively.

House and car insurance about $500/month (assuming no kids car on your insurance, else add $250/kid)

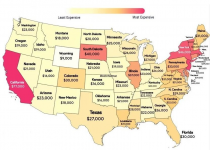

If you live in central Tx and want to stay here, that's $1000/month property tax

Then add $800/month for water/electricity/services/phones/internet

So that's $3500-4500/month BEFORE EATING if you try to retire and pay for everything on your own.

And I do want to pass some onto my kids, not sure how they are gonna afford a house otherwise (but wife keeps telling me they'll be fine).

I do think $5mil is way more than enough to retire mid-50s without health care paid for, but that $2mil can sure disappear with a couple of decent vacations and the occasional new car. And $1mil is a non-starter for early retirement.

OT - Retirement discussion - what is the least amount of $$ needed to retire?

- Thread starter dawgstudent

- Start date

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

My personal off-ramp is just cutting back on hours at my regular job. I’m down to about 1,400 hours per year now. I could retire but I like what I’m doing & the people I work with. So I’ll stay at it for another year or two.^ this

Trying to think of a lifestyle type business to start as an exit ramp. Let's say it's consulting then you build it around your life using your earned professional relationships, expertise, etc. Take the jobs you want to work. If it involves travel double up with a vaca at the back end or front end. Just needs to drive a little income to keep from dipping into your savings too much and would also give some purpose to your "free time."

Also, thought about some kind of relatively safe franchise model that I could eventually get the kids involved in. That could provide a lot of tax advantages.

Well intended thoughts but no action yet***

I’ve been told by multiple legislative leaders that they have legal responsibility to maintain PERS to retirees. Otherwise they would lose in court. They would make cuts if they could. In other words the State of Mississippi would have to become insolvent to make changes. I do believe that they will continue to make changes for new public employees which they did this session.Private pensions are not risk free, but I think ERISA has mostly fixed companies raiding or not funding their pensions, so they are pretty safe until their is a complete breakdown in the rule of law. At least as safe as 401k's.

But things like PERs and Social Security, where a government has promised to tax people in the future to pay you benefits in the future are definitely at risk. Social security will at least be funded at something like 75%, so I would think you won't take more than a 50% or 60% cut (assuming they cut high earners to avoid cutting low earners). But PERS is more like private plans, where it's hard legally to cut payments before the money is just gone. Don't know what's going to happen when there are no assets and taxpayers are just asked to pay a bunch of retirees a **** ton of money because some irresponsible legislators in the 90's said they would.

I have most of my retirement with Edward Jones. Their app has a “play” page. Once you get all your information put in and a plan established then you can change things such as frequency of purchasing cars, adding a travel budget, buying a new home, basically what if scenario’s . This allows you to see what expenses now do to you 25-30 years down the road. It’s really educational and enlightening. My plan is assuming that I die at 89. The difference between running out of money before I die and leaving someone over 5 million dollars is only about $35,000 per year in spending.

Mine are just barely under that, but not by much. Texas gotta get their monies.$1,000/month property taxes? Wow!

She should consider a Roth conversion if her intent to pass it on.Yeah, my mom gets an RMD auto deposit that turns out to be not needed, except to pay the extra income taxes associated with it. Pain in the @$$.

They showed us the projected revenue from that back in the Fall of last year, and it honestly wasn't that much. The gaming lobby killed that bill. They want you in the casinos, for obvious reasonsI'd legalize mobile sports gambling and use some of these proceeds (taxes) to shore up PERS.

i would retire but i bought a big super crew F150 king ranch lifted it wouldn’t go in my garage so I just made a lounge out of the garage with a bar, leather furniture and a killer golf simulator. Now I have to work and pay for all this stuff******. Actually retired at 57. to be safe you need 3 million but 5 makes life easy

PERS was changed for all new enrollees, in this past legislative session. A 5th tier was created. It's basically like any other 401K that a private company would offer. It's not a fix for PERS, but it's a start. All new hires after March 15th of 2026 fall into that new level of PERS. When baby boomers die off in the next 15-20 years, some relief will be seen.I don’t know that cutting social security will ever be politically possible. There’s a lot of old voters & even more coming. PERS benefits can’t be cut retroactively. They can, and should, change the benefit formula going forward. Full retirement after 25 years is insane.

fyi: They showed us the numbers for the HB1 income tax elimination bill at our MS Association of Supervisors convention in June and current projections show that it will be 29 years before it's completely eliminated.

Correct. The 13th check is supposed to be a COLA payment each year so it grows. For many it becomes a large part of what the ey make off PERS. Absolutely none of the math maths.I have no idea how the PERS retirement works, but my wife is a school teacher and she's grandfathered in where she can retire after teaching for 25 years. This will be her 17th year teaching. Is that when the 13th check comes in to play when she decides to retire?

I intend to have enough where it's still growing after I retire. I'm not interested in my last check bouncing.

So I guess probably double whatever I "could get by on".

So I guess probably double whatever I "could get by on".

I hope not. That’s so small in the context of the problem I’m not sure it even counts as a bandaid. If we’re not going to fix it, I’d rather not keep dumping taxpayer money into it to end up at the same spot. If haircuts are coming, that $300M should be spread over all the pers recipients to mitigate everybody’s pain rather than favor older participants rather than younger ones.In the ‘26 session, I look for the legislature to move at least $300,000,000 of the surplus they are sitting on to PERS to shore it up near term. That will buy some more time to completely kick the can down the road.

I rolled over my PERS account and bought bitcoin at $30k in an IRA (holding the private keys myself).I cashed my wife’s out for that reason.

Three states have passed strategic bitcoin reserve bills. Eight more have pending legislation.In the ‘26 session, I look for the legislature to move at least $300,000,000 of the surplus they are sitting on to PERS to shore it up near term. That will buy some more time to completely kick the can down the road.

Will Mississippi be the last state to do this?

Here’s a pretty good calculator I used before I retired to run my numbers through. There’s a simple ballpark version…..and one you can get down and dirty with a lot of details.

www.firecalc.com

www.firecalc.com

FIRECalc: A different kind of retirement calculator

Y’all better be running these numbers with NIL contributions included in your budgets. If you delay retirement by one year, you can buy us a DB for one season.

My plan ties mobile sports betting to a MS land based casino.They showed us the projected revenue from that back in the Fall of last year, and it honestly wasn't that much. The gaming lobby killed that bill. They want you in the casinos, for obvious reasons

I’ll get the bulldog club to call you soon.My personal off-ramp is just cutting back on hours at my regular job. I’m down to about 1,400 hours per year now. I could retire but I like what I’m doing & the people I work with. So I’ll stay at it for another year or two.

Hi DadI hope to leave a substantial legacy for my kids and so far I’m well above plan on that goal and we are thoroughly enjoying retirement.

The good news is if you live in Mississippi, the retirement money doesn’t have to last as long.

Don’t think that it went unnoticed that you didn’t mention a “good” DBY’all better be running these numbers with NIL contributions included in your budgets. If you delay retirement by one year, you can buy us a DB for one season.

* And more importantly, your surviving familyWith everything paid off it's still suprising how many expenses you still have. Insurance, taxes, gas, utilities, a new vehicle from time to time, travel,,ect. Y'all can add to the list ,but something you don't think about when your fairly young and healthy is long term care. It can break you.

This is always the mega conundrum for me. Now that all of our parents and step parents have crossed 70, that sure seems like magic number when even light travel starts to become a significant burden.As far as health goes I have research and figured age 64 is prime age. You still have about six years of good health to travel and do things you want to do when you retire.

I’ve always been one to prioritize financial security over many other things, but the uncertainties surrounding health in our later years is really making me want to target 60 for retirement

Yeah, between my wife and I, we have 7 combined parents and step parents. There are only two of them that have any kind of savings, and the rest are essentially living off of SS and minimal pensions.I guess define normal.

If I was in retirement and house paid off and no kids and no need to save additional each month, $5,000/month after tax would go a long way. I can break that out for the naysayers. That’s for a single man.

Obviously you wouldn’t have a ton of money for vacations and such but you could do stuff.

husband and wife? $6500.

Based on what you read today, you’d think that what I just wrote was the beginning of a horror story, but they’re all doing completely fine. Sure, they’re not taking European cruises, but they’re enjoying life. To me, one of the most crucial retirement mistakes these days is going into it alone. Sometimes that can’t be helped, but the ability to share expenses, household chores, and to simply have a companion is so important

Now we know why our NIL is dead last. Every other school is trying to win football games while these MFers are trying to retire…It looks like only about 2.5% of the population have over a million in their 401k. Only 25 percent or so of those 55-64 has 250k.

The Pack has exceptional investing skills apparently!

Sure, but when those other fans get up and go to work at age 85 they will have the satisfaction of helping land the 14th best right guard in the country. Why, without him they never would have made the Reliaquest Bowl that year. And sure, the RG wasn't in Tampa since he sat out before the bowl game and transferred to Texas Tech but you simply cannot take away the memories made along the way.Now we know why our NIL is dead last. Every other school is trying to win football games while these MFers are trying to retire…

That 60% number passes the sniff test for me, but I have to imagine that the vast majority of that figure is tied up in primary dwellings, and I don’t really consider that to a liquid retirement asset. Sure, some like to downsize in retirement, and you could make some money by doing that, but people have to live somewhere, right?

**And it isn’t gonna be our spare bedroom if my Mil is reading

**And it isn’t gonna be our spare bedroom if my Mil is reading

So if I donate and delay retirement I get to watch us in the Reliaquest Bowl? Sign me up.Sure, but when those other fans get up and go to work at age 85 they will have the satisfaction of helping land the 14th best right guard in the country. Why, without him they never would have made the Reliaquest Bowl that year. And sure, the RG wasn't in Tampa since he sat out before the bowl game and transferred to Texas Tech but you simply cannot take away the memories made along the way.

Yep, I see a lot of this too, and I suspect that it’s a little of both when it comes to wanting to work versus needing to work. Certainly, someone making $300k+ didn’t get there by twiddling his thumbs, and I can see how the thought of a quiet retirement life may be nerve wracking.I know a lot of people that still work pretty hard in their 60's after making good money for a long time. I actually know very few people not hitting a milestone for a pension that retire at 62 or even 65. I'm always curious as to how much of that is just recognizing that they're not going to like retirement versus actually needing to work because they can't afford to retire. .

I feel like there are a lot of single earner families where the dad makes between $250k and $450k and they spend $300k putting three kids through private elementary and high school, and then ramp up their spending on cars, vacations, and college to whatever level ensures the dad is going to have to work until 70 to maintain their lifestyle.

That said, I think that it’s more commonly the latter where somewhere in that 40-60 age range, mom and dad got really comfortable with their lifestyle, and $2M in retirement funds may be good money, but it won’t let you keep that way of life going.

That 60% number passes the sniff test for me, but I have to imagine that the vast majority of that figure is tied up in primary dwellings, and I don’t really consider that to a liquid retirement asset. Sure, some like to downsize in retirement, and you could make some money by doing that, but people have to live somewhere, right?

**And it isn’t gonna be our spare bedroom if my Mil is readingThere is. Saying “you can’t eat your house.

There is a saying ”you can’t eat your house.” Although it helps cash flow to have it paid off, if you need it, the equity isn’t normally cheap to get at. Selling isn’t quick or cheap and HELOCS, reverse mortgages have fees and high rates. As much as there is a desire for me to be mortgage free, at 2.5% it doesn’t make sense when I can still get a CD close to 5%, so I just out any extra that I would pay towards the mortgage in them up until the rate drops below the mortgage cost.That 60% number passes the sniff test for me, but I have to imagine that the vast majority of that figure is tied up in primary dwellings, and I don’t really consider that to a liquid retirement asset. Sure, some like to downsize in retirement, and you could make some money by doing that, but people have to live somewhere, right?

**And it isn’t gonna be our spare bedroom if my Mil is reading

There's a lot of variable so there's no "one size fits all" answer here.

With that said, I think most people should be able to retire comfortably with $1 - $1.5 MM.

With that said, I think most people should be able to retire comfortably with $1 - $1.5 MM.

Where do you invest your retirement funds after retirement? They need to be protected from market volatility, right?My wife and I retired 6 years ago at age 64 so we have some experience with this. It depends on a few things. Overall health, retirement plans for traveling, desire to still eat at restaurants on a regular basis, family responsibilities, etc. everyone has different wants and needs. Figure out what you spend per month now, how much you want to spend for entertainment, healthcare cost, etc. then decide how much income you need above social security and any other steady income you have, like a pension for example. Then decide how much additional savings you need to draw from. Just make a spread sheet and put it all down in black and white. Don’t forget that you will still need a new vehicle occasionally and nursing homes are currently running around $10,000 per month. To be fair to your children, you need to plan to live to 100, even though most people don’t make it. You don’t want to become a burden to them. With all of that being said, I expect that you will decide that you are going to need $2-3 mil in most cases. Your going to want to be a bit more conservative with investing to protect your available cash stream against the unexpected, like Covid or a 9-11 type of event crashing the market for a few years. If you do your homework and plan correctly it is a wonderful reward for all of your years in the workplace. We travel, go on western hunting trips, and pretty much do whatever we want too only because we planned correctly. I know other retired people who are restricted from doing anything other than going to Kroger and complaining about the price of potato salad. DETAILED PLANNING IS THE KEY!

PERS cannot be cut legally but they PERS obligations can't be paid because of math, and laws can't overrule math. We had a chance to fix PERS and we didn't. It would have been painful, but doable. Now we've let the unfunded liability grow to more than three times our annual spending. Any taxes that would let us get it funded at this point would put us into a downward spiral. We should be setting aside a pot of money to be made available if and when there is a solution. Instead of putting $300m into a blackhole, we should set it aside in restricted cash and try to add to it each and every year to be made available if and when we have a mechanism to fix it going forward. A few billion in haircuts Haircuts by the retirees plus a few billion set aside over the years plus a few billion in promised upped contributions from the state and you don't even get the problem half fixed, so even putting $300M a year aside may be relatively pointless, but at least it would be something to lessen the blow when we have to face reality.I’ve been told by multiple legislative leaders that they have legal responsibility to maintain PERS to retirees. Otherwise they would lose in court. They would make cuts if they could. In other words the State of Mississippi would have to become insolvent to make changes. I do believe that they will continue to make changes for new public employees which they did this session.

The alternative is to just wait until it collapses under its own weight and have nothing to lessen the blow. It will just be PERS recipients arguing that they were promised these benefits and the state should levy confiscatory property taxes (because that's the only thing we can really tax that won't move) and non-recipients arguing that they didn't sign up to guarantee those payments and the workers took the risk working for an unfunded pension. Neither side will be wrong and there will be no fair way to resolve it at that point, and us trying to kick the can down the road just makes the problem bigger.

The gaming lobby claims they are good with a bill that requires the bets to go through an app tied to a physical casino in the state, and that the bill was killed by legislators fighting over how the revenue would be split. Not sure they were super disappointed it failed and maybe certain legislators took an unreasonable stance on revenue split to kill it without killing it "for the casinos", but at least publicly the gaming lobby was not against it.They showed us the projected revenue from that back in the Fall of last year, and it honestly wasn't that much. The gaming lobby killed that bill. They want you in the casinos, for obvious reasons

If I convert my annual state income tax liability to a monthly cost and add that figure to my annual ad valorem tax liability converted to a monthly cost, I am under $1,000/month for BOTH. I have a great CPA who maximizes my income tax avoidance and my house is pretty modest for my income level, but it goes to show that states with zero income tax will rape and pillage for revenue. And states will shift the burden of tax revenue onto local political subdivisions. This is what will ultimately happen in Mississippi if there is ever a complete elimination of state income tax. Your ad valorem taxes will be increased dramatically to offset the revenue lost.$1,000/month property taxes? Wow!