Yuup. My house is two story and 3000 (ish) SF. USAA paid me $27k for a new roof in 2022.got up to that $22,000 number on the second one. I think that’s a pretty typical cost for midsized home.

Last edited:

Yuup. My house is two story and 3000 (ish) SF. USAA paid me $27k for a new roof in 2022.got up to that $22,000 number on the second one. I think that’s a pretty typical cost for midsized home.

He means that someone basically committed insurance fraudWhat do you mean the “roofer ate the deductible”?

I didn't pay anything. He sent the quote to the agent. The adjuster came out and looked at it. Farm Bureau sent me a check for 20K I endorsed it over to him once the job was completed. Then Farm Bureau game me 700.00 check as a refund of premium. New roof lower premium,Did you get a quote up front or just give him the check?

It's not the square foot of the house it's the tall roof that I have with a lot of footage and the type of roof as well. Architectual Singles are not cheap.Holy Crap, 22k to replace a roof? How many sq feet is it?

I don't know where you live but there is a is a lot of competition here in Rankin County Miss. So, they do what they have to do to get the business. Farm Bureau agreed with the roofer. Miss Farm Bureau is one of the best Mutual Fire companies in the state and they take care of their Farm Bureau Members.Actually only $20k evidently****

I will say I’ve done two roof / gutter replacements in the past 10 years….first was out of pocket on a 2000sf house in 2016 or so, second was through insurance on a 3500sf house in 2023. The cost per sf was around the same both times, got up to that $22,000 number on the second one. I think that’s a pretty typical cost for midsized home.

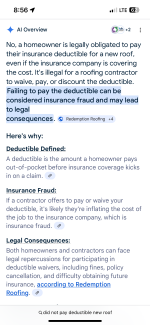

You would think so but apparently not. It’s pretty common for roofers to eat the deductible or upgrade you from regular shingles to architectural ones. As long as the insurance company cost aligns with the adjusters cost they’re ok with it.He means that someone basically committed insurance fraud

You are absolutely correct. They sent their adjuster out to look at the roof after the roofer quoted and he agreed with the roofer about the cost. The deductible was between me and the roofer not the roofer and Farm Bureau. He wanted my business. Business cut deals all the time in all walks of life to get business. Heck he might have taken a tax deduction off it.You would think so but apparently not. It’s pretty common for roofers to eat the deductible or upgrade you from regular shingles to architectural ones. As long as the insurance company cost aligns with the adjusters cost they’re ok with it.

I don’t care how he does it. It is 100 percent fraud for the roofer to eat the deductible. And of course it happens all the time, under the table. But insurance gives you ACV money up front during a roof replacement. When you get your roof finished, you and/or your contractor has to submit a cert of completion along with a final invoice (what you were charged for the roof). Then they’ll release the depreciation and whatever supplements the contractor added, if they got approved.You would think so but apparently not. It’s pretty common for roofers to eat the deductible or upgrade you from regular shingles to architectural ones. As long as the insurance company cost aligns with the adjusters cost they’re ok with it.

Actually the deductible is between you and farm bureau. The contractor has no say in it at all, legally speaking.You are absolutely correct. They sent their adjuster out to look at the roof after the roofer quoted and he agreed with the roofer about the cost. The deductible was between me and the roofer not the roofer and Farm Bureau. He wanted my business. Business cut deals all the time in all walks of life to get business. Heck he might have taken a tax deduction off it.

I can choose my deductible with the insurance company but what I pay out of my pocket which is the deductible I can negotiate with the roofer. Farm bureau said I owed 2000K of the 22K. I negotiated that 2000 down to 0 with the roofer.Actually the deductible is between you and farm bureau. The contractor has no say in it at all, legally speaking.

Farm Bureau is one of the better ones in AL as well….allegedly. Them and Alfa are good for roofs.I don't know where you live but there is a is a lot of competition here in Rankin County Miss. So, they do what they have to do to get the business. Farm Bureau agreed with the roofer. Miss Farm Bureau is one of the best Mutual Fire companies in the state and they take care of their Farm Bureau Members.

I don’t think the cost number you threw out there was out of line, tall roof or not.It's not the square foot of the house it's the tall roof that I have with a lot of footage and the type of roof as well. Architectual Singles are not cheap.

Alabama Life Farmers Association is Part of the Farm Bureau Federation in Alabama. Shelter is a smaller company out of Missouri, but they are pretty good as well.Farm Bureau is one of the better ones in AL as well….allegedly. Them and Alfa are good for roofs.

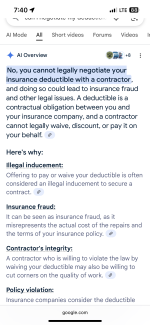

No you cannot negotiate it. That 22k amount is the Replacement cost to complete your roof that was agreed upon by the contractor and farm bureau. Your deductible is included in that 22k.I can choose my deductible with the insurance company but what I pay out of my pocket which is the deductible I can negotiate with the roofer. Farm bureau said I owed 2000K of the 22K. I negotiated that 2000 down to 0 with the roofer.

The one question I would have if my contractor offered to eat the deductible is how many corners is he going to cut to make that up. When I had my roof replaced, I paid the full deductible.No you cannot negotiate it. That 22k amount is the Replacement cost to complete your roof that was agreed upon by the contractor and farm bureau. Your deductible is included in that 22k.

No ****! You are arguing words. It is simple and you are making hard. I chose my deductible when I bought my policy. The claim was for 22K. I owed 2K and Farm Bureau owed 20K. Farm Bureau paid their part, and I negotiated with the roofer what I paid out of the 2K remaining and I negotiated that down to zero.No you cannot negotiate it. That 22k amount is the Replacement cost to complete your roof that was agreed upon by the contractor and farm bureau. Your deductible is included in that 22k.

Where they save money is the 15 Mexicans, he hires to put the roof on. I am really good friends with my agent, and I used the roofer he trusted and recommended to me. Trust me after the hailstorm I had 20 different companies come by wanting to put a roof on my house. I stayed away from them. I knew my roof was old and had hailstorm but it was the fact my premium went up because of it is why I acted.The one question I would have if my contractor offered to eat the deductible is how many corners is he going to cut to make that up. When I had my roof replaced, I paid the full deductible.

As far as you’re concerned they all have valid green cards or work visas.Where they save money is the 15 Mexicans, he hires to put the roof on. I am really good friends with my agent, and I used the roofer he trusted and recommended to me.

I asked the roofer about the people putting the roof on and he told me there are about five different groups of Mexicans that put the roofs on. Each group are an independent contractor that the roofing companies hire. I am not saying all companies do it, but he said most use the five different groups. I asked him what if one falls off my roof and gets hurt. He said he is bonded or whatever that means he would be responsible. They really did a good job. I had some face boards that got dry rotted because the roof was old, but I hired a guy to replace those. He was a US Citizen.As far as you’re concerned they all have valid green cards or work visas.

I think you’re the one who doesn’t understand it. You, the homeowner, can not negotiate the deductible amount with the roofer. He is required to charge you that amount. It is required, by law, for you to pay it. If he keeps records of it or is ever investigated then he’ll be the one in trouble. If insurance somehow finds out that you only paid the roofer the checks you received from farm bureau, and didn’t pay your 2k then they will revise their estimate to 20k and change the amount given to you to 18k. Thus making you reimburse them 2kNo ****! You are arguing words. It is simple and you are making hard. I chose my deductible when I bought my policy. The claim was for 22K. I owed 2K and Farm Bureau owed 20K. Farm Bureau paid their part, and I negotiated with the roofer what I paid out of the 2K remaining and I negotiated that down to zero.

Yeah, you 17d up not getting a quote, I got a check from my insurance and made 4k on my roof after Hurricane Michael. I used that money to upgrade additional items on my house.I didn't pay anything. He sent the quote to the agent. The adjuster came out and looked at it. Farm Bureau sent me a check for 20K I endorsed it over to him once the job was completed. Then Farm Bureau game me 700.00 check as a refund of premium. New roof lower premium,

My insurance company was sending out an adjuster and the check was not going to be mailed to me until job was completed. I guess I could have negotiated more with him. It didn't cost me anything and I got a refund on my premium because it went down. I was happy.Yeah, you 17d up not getting a quote, I got a check from my insurance and made 4k on my roof after Hurricane Michael. I used that money to upgrade additional items on my house.

I don't care what you or you team do. Since you know so much I will through some terms at you. I have had my P&C license for 30 years. I have had my Life Accident and Health license for 30 years. All in Miss. I have Life Accident and Health in 11 other states. I used to have series 6 and 63, I let them go when they changed the law keeping you from parking them. I have a CLU, FSCP and a LUTCF designation. All from the American College. The CLU course is harder than any class I took at State. I get the required CE credits every two year to renewal my license. I don't sell anymore and have not for 23 years, but I have to keep my license for job. The only time insurance companies give a **** is when you win a personal injury case from an auto accident and the Medical Insurance company want their money back. Homeowner claims they are going to pay what they owe and done with it. What I did is really no different than me negotiating my out-of-pocket expense with the hospital after a stay. Yes, I have done that. Just make an offer. United Health didn't care either. What I owe is what I owe and that's between me and the roofer.I think you’re the one who doesn’t understand it. You, the homeowner, can not negotiate the deductible amount with the roofer. He is required to charge you that amount. It is required, by law, for you to pay it. If he keeps records of it or is ever investigated then he’ll be the one in trouble. If insurance somehow finds out that you only paid the roofer the checks you received from farm bureau, and didn’t pay your 2k then they will revise their estimate to 20k and change the amount given to you to 18k. Thus making you reimburse them 2k

You picked the wrong person to debate this with btw. My team gets brought in on cases like this all the time. It’s one of the main reasons why premiums are going up. Inflated costs by shady contractors

Congrats on your longevity in insurance. Means zilch. I too have 20 years of p&c, as well as construction law. I’m always amazed at how many agents don’t understand the nuts and bolts of insurance and the law. And especially they don’t know about the claims process. You’re there to sell policies and that’s it.I don't care what you or you team do. Since you know so much I will through some terms at you. I have had my P&C license for 30 years. I have had my Life Accident and Health license for 30 years. All in Miss. I have Life Accident and Health in 11 other states. I used to have series 6 and 63, I let them go when they changed the law keeping you from parking them. I have a CLU, FSCP and a LUTCF designation. All from the American College. The CLU course is harder than any class I took at State. I get the required CE credits every two year to renewal my license. I don't sell anymore and have not for 23 years, but I have to keep my license for job. The only time insurance companies give a **** is when you win a personal injury case from an auto accident and the Medical Insurance company want their money back. Homeowner claims they are going to pay what they owe and done with it. What I did is really no different than me negotiating my out-of-pocket expense with the hospital after a stay. Yes, I have done that. Just make an offer. United Health didn't care either. What I owe is what I owe and that's between me and the roofer.

Well apparently, not in my case. and I'm not an agent anymore. This was between me and the roofer. I seriously doubt the roofer adjusted the estimate after the fact. Too many documents were signed. Anyways you and your team should be really busy because it is happening a lot.Congrats on your longevity in insurance. Means zilch. I too have 20 years of p&c, as well as construction law. I’m always amazed at how many agents don’t understand the nuts and bolts of insurance and the law. And especially they don’t know about the claims process. You’re there to sell policies and that’s it.

And if you don’t think insurance companies care about saving 2k per claim then you’ve lost your damn mind.

It's not that they are intellectually challenged, it's that we allow lobbying. I mean some serious donations are being given to each and every one of them from someone to get something they want passed. Lobbying makes them rich and keeps them from doing what is right.You’re right, there’s no way our federal government could do something like that. Requires Congress to not be intellectually challenged.

I think everything you are saying is kind of proving his point. He didn’t adjust the estimate after the fact because he didn’t have to….he already had enough fluff margin in there to be able to drop $2k off the bottom line, and still have it be well worth the effort.Well apparently, not in my case. and I'm not an agent anymore. This was between me and the roofer. I seriously doubt the roofer adjusted the estimate after the fact. Too many documents were signed. Anyways you and your team should be really busy because it is happening a lot.

Well, I'll make a deal with my insurance company. I'll pay my deductible in full if they don't rob me by depreciating my assets unjustly. Until then, if I have a buddy who owns a roofing company and can work with him to minimize the impact of the deductible, I'm doing that, and I'll sleep well at night. The last thing I'm worried about is an insurance company being defrauded. They do a helluva lot more defrauding than getting defrauded.I don’t care how he does it. It is 100 percent fraud for the roofer to eat the deductible. And of course it happens all the time, under the table. But insurance gives you ACV money up front during a roof replacement. When you get your roof finished, you and/or your contractor has to submit a cert of completion along with a final invoice (what you were charged for the roof). Then they’ll release the depreciation and whatever supplements the contractor added, if they got approved.

Insurance is expecting you to pay your deductible. If you submit a final invoice to insurance that is less than what the estimate is then insurance will reduce the amount being sent in the depreciation to match. So you have contractors send in an invoice that matches the original estimate and tell the homeowner on the backend you only have to pay me “X” amount so you can keep the rest.

You had me at "release the depreciation".I don’t care how he does it. It is 100 percent fraud for the roofer to eat the deductible. And of course it happens all the time, under the table. But insurance gives you ACV money up front during a roof replacement. When you get your roof finished, you and/or your contractor has to submit a cert of completion along with a final invoice (what you were charged for the roof). Then they’ll release the depreciation and whatever supplements the contractor added, if they got approved.

Insurance is expecting you to pay your deductible. If you submit a final invoice to insurance that is less than what the estimate is then insurance will reduce the amount being sent in the depreciation to match. So you have contractors send in an invoice that matches the original estimate and tell the homeowner on the backend you only have to pay me “X” amount so you can keep the rest.

Congrats on your longevity in insurance. Means zilch. I too have 20 years of p&c, as well as construction law. I’m always amazed at how many agents don’t understand the nuts and bolts of insurance and the law. And especially they don’t know about the claims process. You’re there to sell policies and that’s it.

And if you don’t think insurance companies care about saving 2k per claim then you’ve lost your damn mind

What you are describing in the personal injury context is called subrogation, and it happens across all insurance lines including P&C if the carrier can find another party responsible for an intervening cause. Of course, that doesn't happen very much because the cause is weather.I don't care what you or you team do. Since you know so much I will through some terms at you. I have had my P&C license for 30 years. I have had my Life Accident and Health license for 30 years. All in Miss. I have Life Accident and Health in 11 other states. I used to have series 6 and 63, I let them go when they changed the law keeping you from parking them. I have a CLU, FSCP and a LUTCF designation. All from the American College. The CLU course is harder than any class I took at State. I get the required CE credits every two year to renewal my license. I don't sell anymore and have not for 23 years, but I have to keep my license for job. The only time insurance companies give a **** is when you win a personal injury case from an auto accident and the Medical Insurance company want their money back. Homeowner claims they are going to pay what they owe and done with it. What I did is really no different than me negotiating my out-of-pocket expense with the hospital after a stay. Yes, I have done that. Just make an offer. United Health didn't care either. What I owe is what I owe and that's between me and the roofer.

The odd thing is I’m definitely not on the insurance’s team. I’ve seen far worse from their side. I say stick it to them when you can because they are definitely not looking out for your best interest.Well, I'll make a deal with my insurance company. I'll pay my deductible in full if they don't rob me by depreciating my assets unjustly. Until then, if I have a buddy who owns a roofing company and can work with him to minimize the impact of the deductible, I'm doing that, and I'll sleep well at night. The last thing I'm worried about is an insurance company being defrauded. They do a helluva lot more defrauding

My house is about the same size. New roof, with metal drip edge and ice/water around the perimeter, was something over $17,000. The top of the line architectural shingles are advertised to be treated against the black streaks you get on the north side. So far, that works after almost 2 years. The roofer used Mexican roofers who worked from sunup to sundown, fearless when working on my 12/12 and 18/12 roof. I don't know if they were legal or not, but only one spoke any English at all. The company was recommended by my State Farm agent.Yuup. My house is two story and 3000 (ish) SF. USAA paid me $27k for a new roof in 2022.

When I pay cash to my mechanic, it's between me and him, because if he told the government that he was not reporting the income and he was not charging me sales tax (that he's not paying) in order to incentivize cash payments, he'd get in trouble.Well apparently, not in my case. and I'm not an agent anymore. This was between me and the roofer. I seriously doubt the roofer adjusted the estimate after the fact. Too many documents were signed. Anyways you and your team should be really busy because it is happening a lot.

This scenario would be a disaster.

If the loser pays the winner's fees every time, legitimate cases that would improve consumer safety will never make it to court because individuals wouldn't be able to take the risk.

Despite cases being very legitimate, there is still a real risk of not winning. Many(most?) individuals in this country can't afford to risk that. Half of adults report living paycheck to paycheck.

This whole 'frivolous' BS is exhausting. It's been literal decades of my adult life hearing that term without it having teeth or meaning.

Frivolous cases are dismissed right now. Courts dismiss cases for lacking merit all the time.

Anyways, your scenario would create a disaster for anyone who is in the right but can't afford to chance not getting a favorable decision. You either don't realize that is the end result or you mistakenly think it wouldn't happen often.

Some frivolous claims are dismissed, many frivolous claims are not. And attorneys fees are rarely awarded even in frivolous claims. Even when lawyers bring claims that don't (and can't) state a claim or can't get past a summary judgment stage, attorneys fees are rarely assessed if it's not contractual.I mean, you ducked the question after being sanctimonious to me about being specific. You weren't specific. That's fine.

But, prepare to have your mind blown wide open. Every state and federal district has that very system in place; awards of attorney fees to an opposing party defending a baseless claim have existed for decades.

Why don't you try again to articulate some actual specific legislative reforms you'd suggest? And I know you know this, but at the risk of condescending to an expert, changes of this nature to insurance law wouldn't be achieved through "tort reform".

I look forward to the continued robust debate on the merits with a subject-matter expert.

'Frivolous'Some frivolous claims are dismissed, many frivolous claims are not. And attorneys fees are rarely awarded even in frivolous claims. Even when lawyers bring claims that don't (and can't) state a claim or can't get past a summary judgment stage, attorneys fees are rarely assessed if it's not contractual.

There are good arguments in favor of the American Rule. Not having it encourages people to fully litigate relatively small value claims. And also discourages people from bringing claims with merit if they can't risk losing and paying attorneys fees.

We could improve things a lot just by having a little bit of skin in the game. But the reality is defense lawyers and judges don't want cases to dry up either.

That's an argument against the legal system in general, not against improving the legal system. What's the difference between gross negligence and negligence? When is conduct outrageous? You can put descriptions on them but it doesn't make them an objective standard, same as frivolous. And just like the legal system is improved by having some things classified as gross negligence as opposed to ordinary negligence, you could improve the efficiency of the legal system by dismissing more frivolous cases or by adding some costs to frivolous cases that go to verdict.'Frivolous'

Define it. Like objectively define it so cases can be clearly categorized as legitimate or frivolous.

...you can't, because personal opinion plays a role in a lot of instances.

I am not trying to be obtusely difficult, I am trying to help show how the argument for reform continually falls apart when categorization is required.

Double check your limits of liability and exclusions. There's a reason it's half as much.I went to Universal Insurance from Geovera last week and dropped from $6700 to $3500 per year. Living in Florida within a half mile of the beach gets expensive quick.

I'm good, Geovera is an insurance of last resort. I got cancelled after Hurricane Michael and had to get something for my mortgage. I kept them for 1 year then they doubled thier rate on me.Double check your limits of liability and exclusions. There's a reason it's half as much.

That is certainly not my experience. I didn't lose much at any of these stages because I have been fortunate enough to have plenty of clients over my career. But, courts in my jurisdictions do a very good job of dismissing claims that aren't proven. "Frivolous" is not a word used in the actual legal profession by defense or plaintiffs' bars, because it was originally ginned up by chambers of commerce to create bad PR for lawyers.Some frivolous claims are dismissed, many frivolous claims are not. And attorneys fees are rarely awarded even in frivolous claims. Even when lawyers bring claims that don't (and can't) state a claim or can't get past a summary judgment stage, attorneys fees are rarely assessed if it's not contractual.

There are good arguments in favor of the American Rule. Not having it encourages people to fully litigate relatively small value claims. And also discourages people from bringing claims with merit if they can't risk losing and paying attorneys fees.

We could improve things a lot just by having a little bit of skin in the game. But the reality is defense lawyers and judges don't want cases to dry up either.